Allpaanel Withdrawal & Payment Guide – UPI, Bank Transfer & Fastest Payout Methods Explained

Introduction: Why a Clear Withdrawal Process Matters

In the rapidly expanding digital advertising ecosystem, platforms that handle ad revenue for publishers and advertisers must provide a transparent, reliable, and swift payout system. Users expect to see their earnings reflected in their bank accounts or digital wallets without unnecessary delays or hidden fees. Allpaanel recognizes this demand and has built a suite of withdrawal options designed to cater to a wide range of preferences, from traditional bank transfers to the instant convenience of Unified Payments Interface (UPI). This guide walks you through each method, outlines the steps required for a successful payout, and highlights the fastest routes to cash out your earnings.

Understanding the Core Withdrawal Options

Allpaanel’s payout ecosystem revolves around three primary channels: UPI, bank transfers (including NEFT, RTGS, and IMPS), and a limited set of alternative methods such as Paytm or other e‑wallets where applicable. While each channel follows a similar verification process, they differ in processing times, transaction limits, and associated costs. By grasping these nuances, you can select the method that aligns best with your financial workflow and urgency.

UPI – The Fastest and Most Popular Choice

Unified Payments Interface (UPI) has revolutionized real‑time money transfer in India. For Allpaanel users, UPI offers near‑instant settlement, typically within seconds of approval. To withdraw via UPI, you need a registered UPI ID linked to a bank account, such as those issued by Google Pay, PhonePe, or BHIM. The platform imposes a minimum withdrawal threshold (often ₹500) and a maximum per‑transaction cap, which may vary based on your account tier and verification status. Because UPI transactions bypass the traditional interbank clearing system, the speed advantage is unmatched, making it the preferred method for most publishers who need rapid access to earnings.

Bank Transfer – Traditional Yet Reliable

Bank transfers remain a cornerstone for users who prefer direct deposits into their savings or current accounts. Allpaanel supports three main formats:

- NEFT (National Electronic Funds Transfer): Typically processed in batches during banking hours, with settlement times ranging from 2 to 4 hours.

- RTGS (Real Time Gross Settlement): Used for high‑value transfers; funds move in real time during working hours but may be subject to stricter limits.

- IMPS (Immediate Payment Service): Allows 24/7 processing, including holidays, and usually settles within minutes, though some banks impose lower transaction limits.

While bank transfers can be marginally slower than UPI, they offer higher limits and are universally accepted across all Indian banks, eliminating the need for a separate UPI app.

Alternative Payout Methods – When They Apply

Depending on your geographical location, transaction volume, and the particular agreement with Allpaanel, you may have access to other payout avenues such as Paytm wallet credits or prepaid debit cards. These alternatives often come with their own fee structures and processing timelines. For most Indian users, however, UPI and bank transfers cover the majority of use cases, providing both speed and flexibility.

Step‑By‑Step Withdrawal Process

Regardless of the chosen method, the withdrawal workflow follows a consistent pattern: authentication, verification, request submission, and final settlement. Below is a detailed walkthrough for each stage.

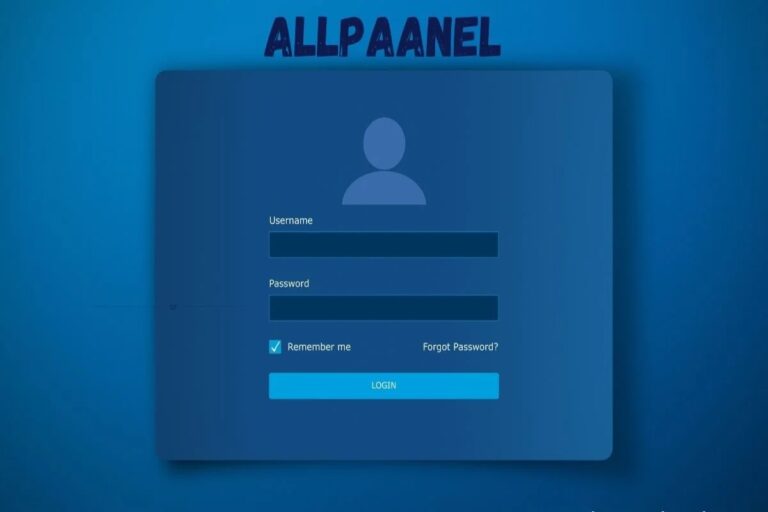

1. Authentication – Secure Access to Your Account

Begin by logging into the platform. Navigate to the dedicated portal at Allpaanel Login. Enter your registered email or mobile number and your password. For added security, enable two‑factor authentication (2FA) if available, as this reduces the risk of unauthorized withdrawal requests.

2. Verification – Ensuring Compliance and Accuracy

Before you can request a payout, Allpaanel requires certain documents to verify your identity and bank details. Typical requirements include:

- A government‑issued photo ID (Aadhaar, PAN, or passport).

- Proof of bank account ownership (a recent bank statement or cancelled cheque).

- If you intend to use UPI, a screenshot of your UPI ID linked to the same bank account.

Upload these documents in the “Verification” section of your dashboard. The review process usually takes 24–48 hours, after which you’ll receive a confirmation email.

3. Request Submission – Choosing the Payout Method

Once verified, navigate to the “Withdraw Funds” tab. Here you’ll see your total available balance, along with the minimum withdrawal amount for each method. Select either “UPI” or “Bank Transfer,” enter the required details:

- For UPI: Your registered UPI ID (e.g., xyz@okaxis).

- For Bank Transfer: Bank name, IFSC code, account number, and account holder name.

Specify the withdrawal amount, adhering to the method‑specific limits. Review the summary, confirm the transaction, and click “Submit.” Some users opt to schedule recurring payouts; the platform supports auto‑withdrawal on a weekly or monthly basis, provided the balance meets the minimum threshold each cycle.

4. Settlement – Tracking the Transfer

After submission, the payout moves into the processing queue. UPI requests typically complete within seconds, and you’ll receive an instant notification on both the platform and your UPI app. Bank transfers may take longer:

- IMPS: Usually within 15 minutes.

- NEFT: Up to 4 hours during banking hours.

- RTGS: Real‑time for amounts above ₹2 lakh, subject to bank operating hours.

You can monitor the status through the “Transaction History” page, which logs timestamps, reference numbers, and settlement confirmation.

Fees, Limits, and Best Practices

Allpaanel maintains a transparent fee structure. UPI withdrawals are generally free of charge, though some banks may levy minor fees on their end. Bank transfers may attract a nominal fee (₹5‑₹15) depending on the chosen process (NEFT vs. IMPS). High‑volume users benefit from reduced or waived fees after meeting certain thresholds.

Withdrawal Limits

Typical daily limits are as follows:

- UPI: Up to ₹1,00,000 per day (subject to bank limits).

- IMPS: Up to ₹2,00,000 per transaction.

- NEFT: No strict daily cap, but each batch may have a maximum of ₹5,00,000.

- RTGS: Minimum ₹2,00,000 per transaction.

Exceeding these limits will result in the request being split across multiple batches, potentially extending settlement time.

Tips for Faster Payouts

To ensure you receive your earnings as quickly as possible, follow these recommendations:

- Keep your profile verified: Incomplete documentation leads to hold‑ups.

- Prefer UPI for small‑to‑medium amounts: Instant settlement with zero fees.

- Schedule payouts during banking hours: NEFT and RTGS are processed only when banks are open.

- Maintain a clean transaction history: Repeated failed withdrawals may trigger a review.

- Use a single, consistent bank account: Switching accounts frequently can delay verification.

Security Considerations When Withdrawing Funds

Financial security is paramount. Always double‑check the bank details or UPI ID before confirming a withdrawal. A typo could send funds to an unintended recipient, and recovery may be complicated. Enable device‑level security such as fingerprint or facial recognition on the platform’s mobile app, if available. Regularly review your transaction logs for any unfamiliar activity and report suspicious behavior to the platform’s support team immediately.

Handling Withdrawal Discrepancies

If you notice a mismatch between the amount you requested and the amount credited, follow this protocol:

- Verify the transaction receipt in your email or platform notification.

- Check your bank or UPI app for the exact amount received.

- Contact Allpaanel support through the “Help Center” with the transaction reference number.

- Provide screenshots of both the platform’s payout confirmation and your bank statement.

- The support team typically investigates within 24 hours and resolves any genuine errors.

Most discrepancies arise from bank‑imposed fees or rounding differences in currency conversion for cross‑border payouts. The platform will clarify any such deductions up front.

Conclusion: Optimizing Your Earnings with the Right Payout Strategy

Effective withdrawal management is a critical component of a successful partnership with any ad revenue platform. By understanding the strengths and limitations of UPI, bank transfers, and alternative payout routes, you can tailor a strategy that balances speed, cost, and reliability. Regularly verify your account details, stay within prescribed limits, and leverage the instant nature of UPI for everyday cash‑outs while reserving bank transfers for larger sums. With these best practices in place, you’ll experience seamless payouts, allowing you to focus on what matters most—creating and monetizing high‑quality content.